Global steel prices start to rise

Global steel prices regained momentum around the market rose again

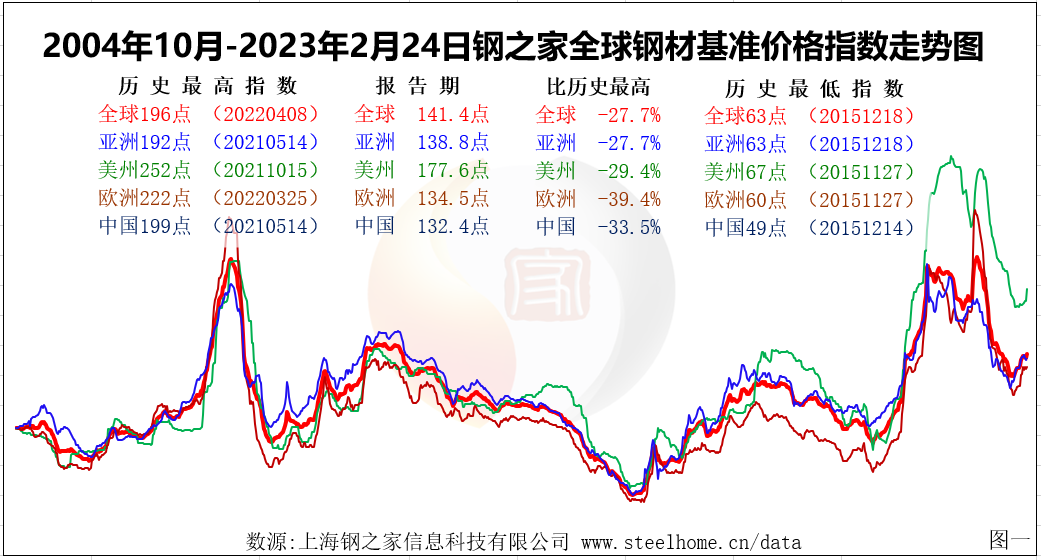

The international steel market shuddered to the upside in February. During the reporting period, the House of Steel Global Steel Benchmark Price Index of 141.4 points rose 1.3% week-on-week (from a decline to an increase), 1.6% month-on-month (unchanged from the previous) and 18.4% month-on-month (unchanged from the previous). The flat steel index was 136.5 points, up 2.2% week-on-week (widening); the long steel index was 148.4 points, up 0.2% week-on-week (turning from down to up); the Asian index was 138.8 points, up 0.4% week-on-week (turning from down to up). In Asia, the China index 132.4 points, up 0.8% week-on-week (from down to up); the Americas index 177.6 points, up 3.7% week-on-week (expanded); Europe index 134.5 points, up 0.8% week-on-week (from down to up).

International steel prices regained their uptrend after a brief correction, largely confirming the previous forecast. From a fundamental point of view, the market around the general upward trend, to the industry has the expectation of unfinished business. From the logic of the operation, the trend after the finishing of the intermediate storage trend, perhaps more aggressive. Especially in the post-epidemic recovery, post-disaster reconstruction, supply reduction and other "bitter" steel needs, the market may go farther, the stage of the high point or will be shown in the near future.

According to the development trend combined with the underlying situation forecast, the international steel market in March or continue to shake upward trend. (See Figure 1)

Global steel production in the first month: down 3.3%; excluding mainland China down 9.3%. WSA data show that: in January 2023, the world included in the WSA statistics of the main 64 countries and regions crude steel production 145 million tons, down 3.3% year-on-year, reducing crude steel production by 4.95 million tons; global (excluding mainland China) steel production 65.8 million tons, a big drop of 9.3% year-on-year, reducing production by 6.72 million tons.

ArcelorMittal plans to restart a blast furnace at its French steel plant. ArcelorMittal said it had decided to restart blast furnace No. 2 at its French steel plant in Fosse-Maritimes in April as European plate prices continued to rebound and the European automotive sector was set to improve in the coming months.

South Korea's POSCO Steel plans to build a new 2.5 million tonne electric furnace. POSCO Steel plans to invest 600 billion won in a new electric furnace and ancillary equipment at its Gwangyang steel plant with a capacity of 2.5 million tonnes of steel per year.

Japan's JFE Steel continues to increase its electrical steel production capacity, and JFE Steel said its new line at the Kurashiki steel plant will be put into production in the first half of fiscal year 2024, when production of non-oriented electrical steel will double.

Faster-than-expected economic restart pushes iron ore prices higher. Goldman Sachs said the latest rise in iron ore prices was largely driven by traders repositioning for a faster-than-expected reboot of the Chinese economy. Goldman also said traders should prepare for a spike in iron ore prices in the second quarter of 2023.

Anglo American's South African high-quality iron ore mines have increased significantly. Anglo American's South African iron ore subsidiary, Kumba Iron Ore, said that rail and port bottlenecks have hindered the movement of iron ore, resulting in a significant increase in the company's high-quality iron ore stocks. As at 31 December, iron ore stocks had increased to 7.8 million tonnes from 6.1 million tonnes in the same period last year.

BHP Billiton is optimistic about the outlook for demand for the commodity. BHP Billiton said it was optimistic about the demand outlook for fiscal 2024, despite the company's lower-than-expected profit in the first half of fiscal 2023 (to the end of December 2022).

FMG accelerates progress on the Belinga iron ore project in Gabon FMG Group signed a mining convention with the Gabonese Republic for the Belinga iron ore project in Gabon. Under the convention, mining will commence at the Belinga project in the second half of 2023 and it is expected to become one of the world's largest iron ore production centres.

Nippon Steel to invest heavily in Canadian mining company. Nippon Steel said it will invest 110 billion yen (approximately RMB 5.6 billion) in a Canadian mining company using raw coal and receive 10% of the common shares. At the same time, with an interest in high-quality raw coal, it will implement and cut CO2 emissions from ironmaking.

Rio Tinto iron ore target cost of US$21.0-22.5 per wet tonne. Rio Tinto reported 2022 financial results saying: Rio Tinto Group 2022 EBITDA of US$26.3 billion, down 30% year-on-year; 2023 iron ore production guidance target of 320-335 million tonnes and iron ore unit cash cost guidance target of US$21.0-22.5/wet tonne.

Korea sets up low-carbon fund to help decarbonise domestic steel industry. South Korea's Ministry of Trade, Industry and Energy said it will set up a fund amounting to 150 billion won (US$116.9 million) to support domestic steelmakers in decarbonising their steel production processes.

Vale supports the construction of a low-carbon and hydro-metallurgical laboratory at CSU. Vale said it will donate US$5.81 million to support a new low carbon and hydrogen metallurgy laboratory ("New Lab") at CSUN. The New Lab is expected to be operational in the second half of 2023 and will be open to all researchers in the mining and steel industries at that time.

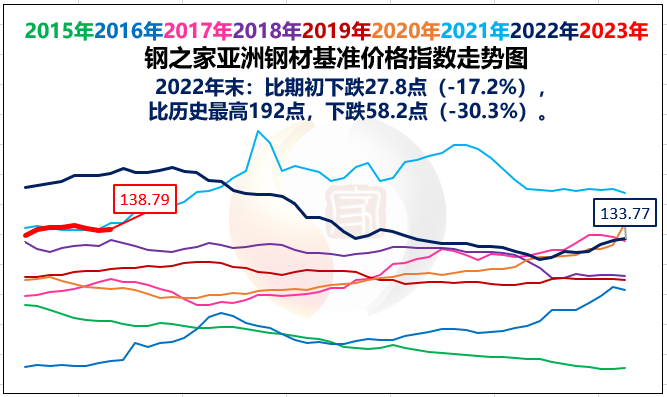

Asian steel markets: steady to up. The 138.8-point Steel House benchmark steel price index for the region rose 0.4% week-on-week (from a decline to an increase), rose 0.6% month-on-month (a convergence of gains) and fell 16.6% month-on-month (a widening of losses). (See Figure 2)

Faster-than-expected economic restart pushes iron ore prices higher. Goldman Sachs said the latest rise in iron ore prices was largely driven by traders repositioning for a faster-than-expected reboot of the Chinese economy. Goldman also said traders should prepare for a spike in iron ore prices in the second quarter of 2023.

Anglo American's South African high-quality iron ore mines have increased significantly. Anglo American's South African iron ore subsidiary, Kumba Iron Ore, said that rail and port bottlenecks have hindered the movement of iron ore, resulting in a significant increase in the company's high-quality iron ore stocks. As at 31 December, iron ore stocks had increased to 7.8 million tonnes from 6.1 million tonnes in the same period last year.

BHP Billiton is optimistic about the outlook for demand for the commodity. BHP Billiton said it was optimistic about the demand outlook for fiscal 2024, despite the company's lower-than-expected profit in the first half of fiscal 2023 (to the end of December 2022).

FMG accelerates progress on the Belinga iron ore project in Gabon FMG Group signed a mining convention with the Gabonese Republic for the Belinga iron ore project in Gabon. Under the convention, mining will commence at the Belinga project in the second half of 2023 and it is expected to become one of the world's largest iron ore production centres.

Nippon Steel to invest heavily in Canadian mining company. Nippon Steel said it will invest 110 billion yen (approximately RMB 5.6 billion) in a Canadian mining company using raw coal and receive 10% of the common shares. At the same time, with an interest in high-quality raw coal, it will implement and cut CO2 emissions from ironmaking.

Rio Tinto iron ore target cost of US$21.0-22.5 per wet tonne. Rio Tinto reported 2022 financial results saying: Rio Tinto Group 2022 EBITDA of US$26.3 billion, down 30% year-on-year; 2023 iron ore production guidance target of 320-335 million tonnes and iron ore unit cash cost guidance target of US$21.0-22.5/wet tonne.

Korea sets up low-carbon fund to help decarbonise domestic steel industry. South Korea's Ministry of Trade, Industry and Energy said it will set up a fund amounting to 150 billion won (US$116.9 million) to support domestic steelmakers in decarbonising their steel production processes.

Vale supports the construction of a low-carbon and hydro-metallurgical laboratory at CSU. Vale said it will donate US$5.81 million to support a new low carbon and hydrogen metallurgy laboratory ("New Lab") at CSUN. The New Lab is expected to be operational in the second half of 2023 and will be open to all researchers in the mining and steel industries at that time.

Asian steel markets: steady to up. The 138.8-point Steel House benchmark steel price index for the region rose 0.4% week-on-week (from a decline to an increase), rose 0.6% month-on-month (a convergence of gains) and fell 16.6% month-on-month (a widening of losses). (See Figure 2)

On the flat steel front: market prices are clearly trending upwards. In India, ArcelorMittal Nippon Steel India (AM/NS India) and JSW Steel both increased prices for hot and cold coils by INR 500/tonne ($6/tonne) with effect from 20 February and 22 February respectively. Following the price increase, hot coils (2.5-8mm, IS 2062) are priced at INR 60,000/t (US$724/t) EXY Mumbai, cold coils (0.9mm, IS 513 Gr O) at INR 67,000/t (US$809/t) EXY Mumbai, medium thick plates (E250, 20-40mm) at INR 67,500/t (US$817/t) EXY Mumbai and medium thick plates (E250, 20-40mm) at INR 67,500/t (US$817/t) EXY Mumbai. / tonne) EXY Mumbai, both excluding 18% GST. In Vietnam, hot coil imports were offered at US$670-685/t CFR, unchanged from the previous price. Ha Tinh Steel announced an increase in domestic hot coils prices for the April delivery period by US$60/t, with the price increase specified at US$699/t (CIF) for de-scaled SAE1006 hot coils and US$694/t (CIF) for non-de-scaled SAE1006 hot coils and SS400 hot coils. In the UAE, HRC imports were assessed at US$680-740/mt (CFR), unchanged from the previous price. Some market sources said $680-690/mt (CFR) for Chinese hot coils and $720-750/mt (CFR) for Indian hot coils. UAE cold coil imports at US$740-760/t (CFR), up US$10-40/t. Hot-dipped galvanised sheet imports at US$870-960/t (CFR), unchanged from the previous price. average export price of SS400 3-12mm hot-rolled coil from China at US$650/t (FOB) in late February, up US$15/t from the previous price. average export price of SPCC 1.0mm cold-rolled coil at US$705/t (FOB), up US$5/t. average export price of DX51D+Z 1.0 mm hot-dipped galvanised coil at US$775/t (FOB), up US$10/t.

In long products: market prices were stable and up. In the UAE, rebar imports were quoted at US$622-641/t (CFR) on a reasonable weight basis, unchanged from the previous price. UAE billet imports were quoted at US$590-595/t (CFR), also unchanged from previous prices. Sources said that UAE mills are generally holding good orders for rebar and overseas billet suppliers are awaiting the latest offers for UAE mills' rebar. In Japan, Tokyo Steel said that its March bar (including rebar) prices would be increased by 3% due to tight market supply. The increase will see the price of rebar rise from 97,000 yen per tonne to 100,000 yen per tonne (about RMB 5,110 per tonne), while prices for other products will remain unchanged. Some analysts say that construction demand in Japan is expected to remain strong in early spring and beyond as many redevelopment projects, manufacturing-related investments and other large projects are launched one after another. In Singapore, rebar was quoted at US$650-660 per tonne (CFR) on a reasonable weight import basis, up US$10 per tonne from the previous price. In Taiwan, China, Sinosteel raised prices by 900-1200 NTD/t (US$30-39.5/t) for medium thick plate and hot rolled coil for March delivery, and by 600-1000 NTD/t (US$20-33/t) for cold rolled coil and hot galvanised. The price increases were mainly necessitated by the continued high prices of raw materials, particularly iron ore which rose by US$2.75 to US$128.75 per tonne (CFR) and Australian coking coal which rose by US$80 per tonne to US$405 per tonne (FOB) in a month, the sources said. In late February, Chinese B500 12-25mm rebar exports averaged US$625/t (FOB), up US$5/t from the previous price.

In terms of trade relations, on February 13, the Indonesian Anti-Dumping Commission said that the anti-dumping duties on H-beams and I-beams originating from China were reviewed at the end of the period.

Brief forecast: According to the operating trend combined with the fundamental situation forecast, the Asian steel market in March or continue to shake upward trend.

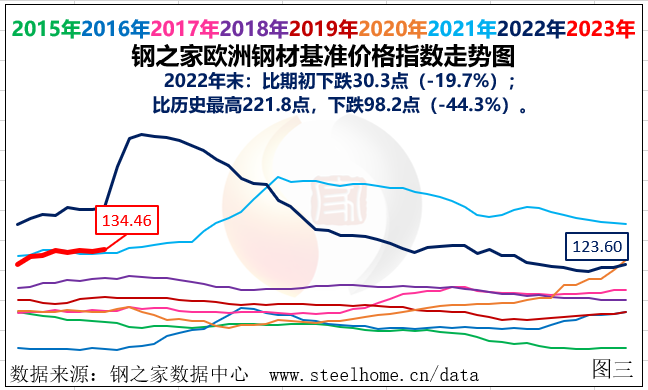

European steel market: continue to rise. The region's 134.5-point Steel House steel benchmark price index, up 0.8% week-on-week (from a decline to a rise), up 3% month-on-month (convergence), down 18.8% month-on-month (expansion of the decline). (See Chart 3)

In flat steel: market prices were more up than down. In Northern Europe, ex-works prices for hot rolled coils were US$840 per tonne, up US$20 per tonne from the previous price. Ex-works cold rolled coils were at US$950/t, unchanged from the previous price. Galvanised sheet was US$955/t, down US$10/t from the previous price. Market sources said that the Nordic mills ex-works offer 800-820 euros per tonne for April and May cargoes of hot coils, which has been raised by 30 euros per tonne from the current price, but the buyers' psychological price is only 760-770 euros per tonne. Some mills said that the April delivery of hot coils orders have been fully booked. Market participants on the March European hot coil prices are expected to rise slightly, the reason is that the European steel mills hot coil orders are generally better, and that buyers will also have the demand for replenishment in March, the steel mill end of the strong willingness to support prices. However, some people said that the terminal demand is not significantly better, the price does not have a reason to rise sharply. In southern Europe, the Italian hot coil ex-factory price of 769.4 euros / ton, up 11.9 euros / ton compared to the previous price. There are Italian steel mills in May cargo period of hot coil ex-works price 780-800 euros / tonne, about equivalent to 800-820 euros / tonne arrival price, up 20 euros / tonne. Some mills said that some pipe makers had placed very good orders for hot coils for the April delivery period and the market continued to look good. In the CIS, hot coil exports were quoted at US$670-720/t (FOB, Black Sea), up US$30/t (FOB, Black Sea) from the previous price. Cold coil exports were quoted at US$780-820/t (FOB, Black Sea), also up US$30/t (FOB, Black Sea). In Turkey, hot coil imports were quoted at US$690-750/t (CFR), up US$10-40/t. Mainstream export offers for hot coils from China to Turkey for the April cargo period were US$700-710/t (CFR). In addition, ArcelorMittal announced a price adjustment of €20/t for May delivery of coil products in Europe, the new prices are: €820/t for hot rolled coil; €920/t for cold rolled coil; and €940/t for hot dipped galvanised coil, all of which are arrival prices. There are industry expectations. Some other European steel mills will also follow suit with price increases.

For long products: market prices continue to rise. In Northern Europe, the ex-works price for rebar was US$765 per tonne, unchanged from the previous price. In Turkey, rebar export prices were US$740-755/t (FOB), up US$50-55/t from the previous price. Exports of wire (low carbon mesh grade) were priced at US$750-780/t (FOB), up US$30-50/t. Sources said that the main reason for steel mills to raise their export offers for long steel is that the reconstruction of the affected areas after the major earthquake is bound to boost domestic demand for long steel and also prices. In fact, after the earthquake, Turkish steel mills have generally raised domestic rebar offers: rebar domestic ex-works price of $885-900 per tonne, up $42-48 per tonne; wire rod domestic ex-works price of $911-953 per tonne, up $51-58 per tonne.

Brief estimation: According to the running trend combined with the fundamental situation forecast, the European steel market in March or continue to shake up the trend.

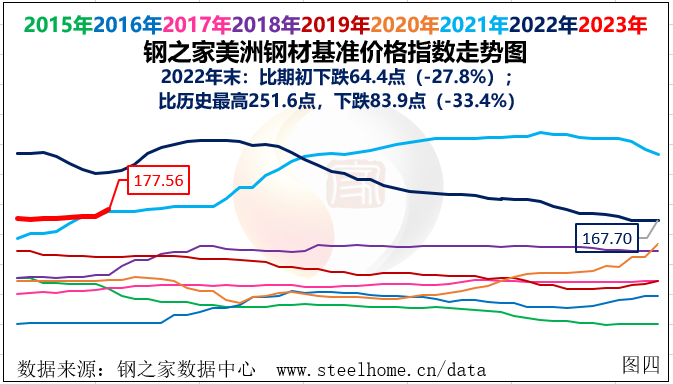

Steel markets in the Americas: up sharply. The region's 177.6-point Steel House steel benchmark price index rose 3.7% week-on-week (up by an extended margin), up 2% month-on-month (up by an extended margin) and down 21.6% month-on-month (down by a converging margin). (See Figure 4)

In flat steel: market prices rose sharply. In the US, ex-works prices for hot-rolled coils were US$1,051/t, up US$114/t from the previous price. Ex-works prices for cold rolled coil were US$1,145/t, up US$100/t. Medium thick plate was US$1,590/t, unchanged from the previous price. Hot-dip galvanised at US$1,205/t, up US$80/t. Following a base price increase of US$50/short tonne (US$55.13/tonne) for plate products by Cleveland-Cliffs in the US, NLMK's US subsidiary also announced a base price increase of US$50/short tonne for hot coils. Some market sources said that most of the US steel mills in April and May period of the hot coil orders received the situation is quite good, and the plant inventory is also declining, so the will to continue to support prices are relatively strong. In South America, hot coil imports were quoted at US$690-730 per tonne (CFR), up US$5 per tonne from the previous price. Mainstream export offers for Chinese hot coils to the Pacific coast countries of South America were US$690-710/t CFR. Import offers for other types of plate in South America: $730-770/t (CFR) for cold coils, up $10-20/t; $800-840/t (CFR) for hot-dipped galvanised sheet, $900-940/t (CFR) for zinc aluminised sheet and $720-740/t (CFR) for medium thick sheet, all broadly unchanged from previous prices.

In long products: market prices were broadly stable. In the US, rebar ex-works prices were US$995/t, broadly unchanged from previous prices. Import prices of US$965/t (CIF) for rebar, US$1,160/t (CIF) for wire rod and US$1,050/t (CIF) for small sections were all broadly unchanged from previous prices.

On trade relations. The US Department of Commerce issued a notice stating that it had decided to impose countervailing duties on China and South Korea's fixed-foot medium thick plates respectively, maintaining countervailing rates of 251% and 4.31%, with the decision taking effect from 15 February 2023.

Brief test: According to the running trend combined with the fundamental situation forecast, the American steel market in March or continue to firm up the trend.